How Nigeria Became Africa’s Fintech Capital — And What’s Coming Next

Ten years ago, sending money to your mother in Owerri required either a trip to the bank, a POS operator with unreliable network, or handing cash to someone who was travelling. Today, it takes approximately eleven seconds and a thumb print. That shift — quiet, unglamorous, and genuinely transformative — is the Nigerian fintech story, and it is one of the most remarkable economic evolutions on the continent.

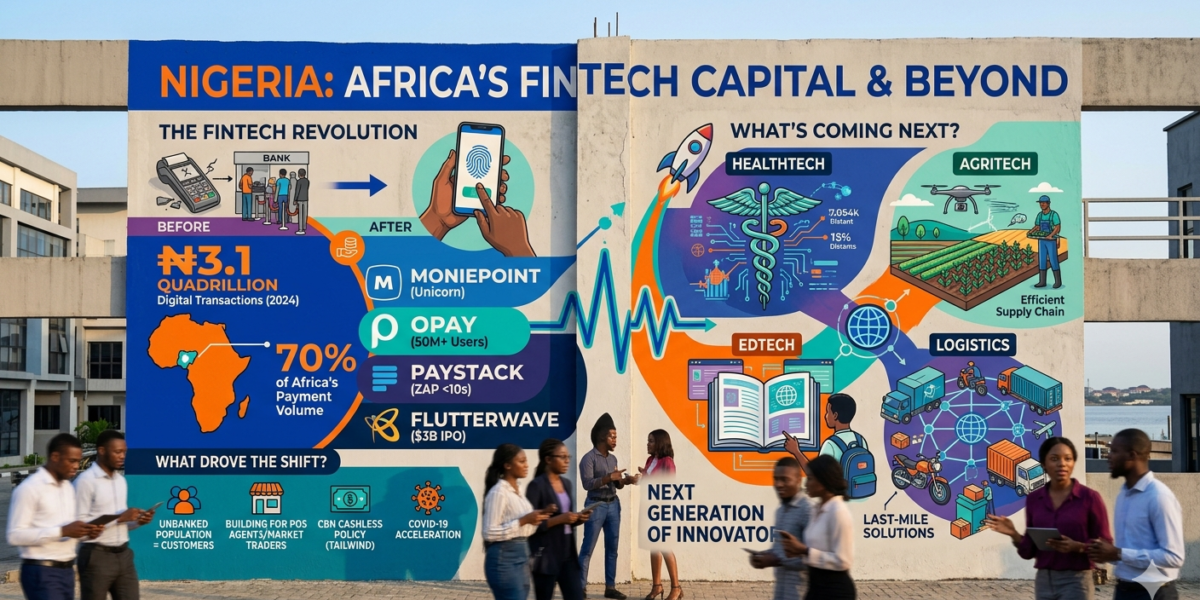

The numbers are staggering when you actually look at them. In 2024, Nigeria processed ₦3.1 quadrillion in digital transactions — that is not a typo. Over 70% of Africa’s total electronic payment volume passed through Nigerian platforms. Moniepoint became a unicorn. OPay hit 50 million users and processes over $12 billion in transactions monthly. Paystack was acquired by Stripe for $200 million and then launched Zap, which moves money between Nigerian accounts in under 10 seconds. Flutterwave is reportedly preparing for an IPO valued at $3 billion. By early 2025, there were over 430 licensed fintech players operating in Nigeria.

What drove this? A combination of factors that nobody planned but everyone benefited from. Nigeria had tens of millions of people with mobile phones and no bank accounts — the exact population that traditional banks had decided was not worth serving. Fintech looked at those people and saw customers. They built for the POS agent in Onitsha market. They built for the small chop seller who needed to receive transfers. They built for the trader in Aba who was previously invisible to the formal financial system.

The legacy banks, comfortable in their marble lobbies and quarterly fees, largely did not see it coming until it had already happened. By the time they noticed, fintechs were handling more than half of Nigeria’s digital transactions. The CBN’s 2012 cashless policy, widely mocked at the time, turned out to be the regulatory tailwind that the industry needed. COVID accelerated everything — mobile money transactions in Nigeria doubled in 2020 alone.

So what comes next? The sectors that look most likely to see similar disruption in the coming years are interesting to watch. Healthtech is the most obvious — Nigeria’s healthcare system has the same structural gap that banking had: a massive underserved population and almost no digital infrastructure serving them. AgriTech is another — Nigeria has enormous agricultural potential and almost no modern supply chain connecting farmers to markets efficiently. EdTech, ironically, given what we just discussed about WAEC results, is a space where digital solutions could genuinely move the needle if they reach the students who need them most. And logistics — the chaos of last-mile delivery in Nigerian cities is a problem so large and so persistent that whoever cracks it properly will build something significant.

Nigeria has proven it can build world-class technology companies. Flutterwave, Paystack, Moniepoint and OPay are not local success stories — they are global ones. The question now is whether the ecosystem matures fast enough to make those next breakthroughs happen from within Nigeria rather than waiting for external capital and external founders to identify the opportunity first.

The fintech decade happened because a generation of Nigerians decided to solve a Nigerian problem with Nigerian ingenuity. The next decade belongs to whoever does the same thing in healthcare, agriculture, logistics and education. The template already exists. Someone just has to use it.